“At the time of difficulties for the SMEs, liquidity is the lifeblood. This is very important.” – Paul Chan, Financial Secretary of the Hong Kong SAR

As explored in our article “New Relief Measure During the COVID-19 Pandemic: Hong Kong Launches the Employment Support Scheme”, The Hong Kong Government have provided substantial financial support to combat the negative economic impacts of COVID-19. As part of the second round of the anti-epidemic Fund, HK$50 billion will go towards the SME Financing Guarantee Scheme (SFGS).

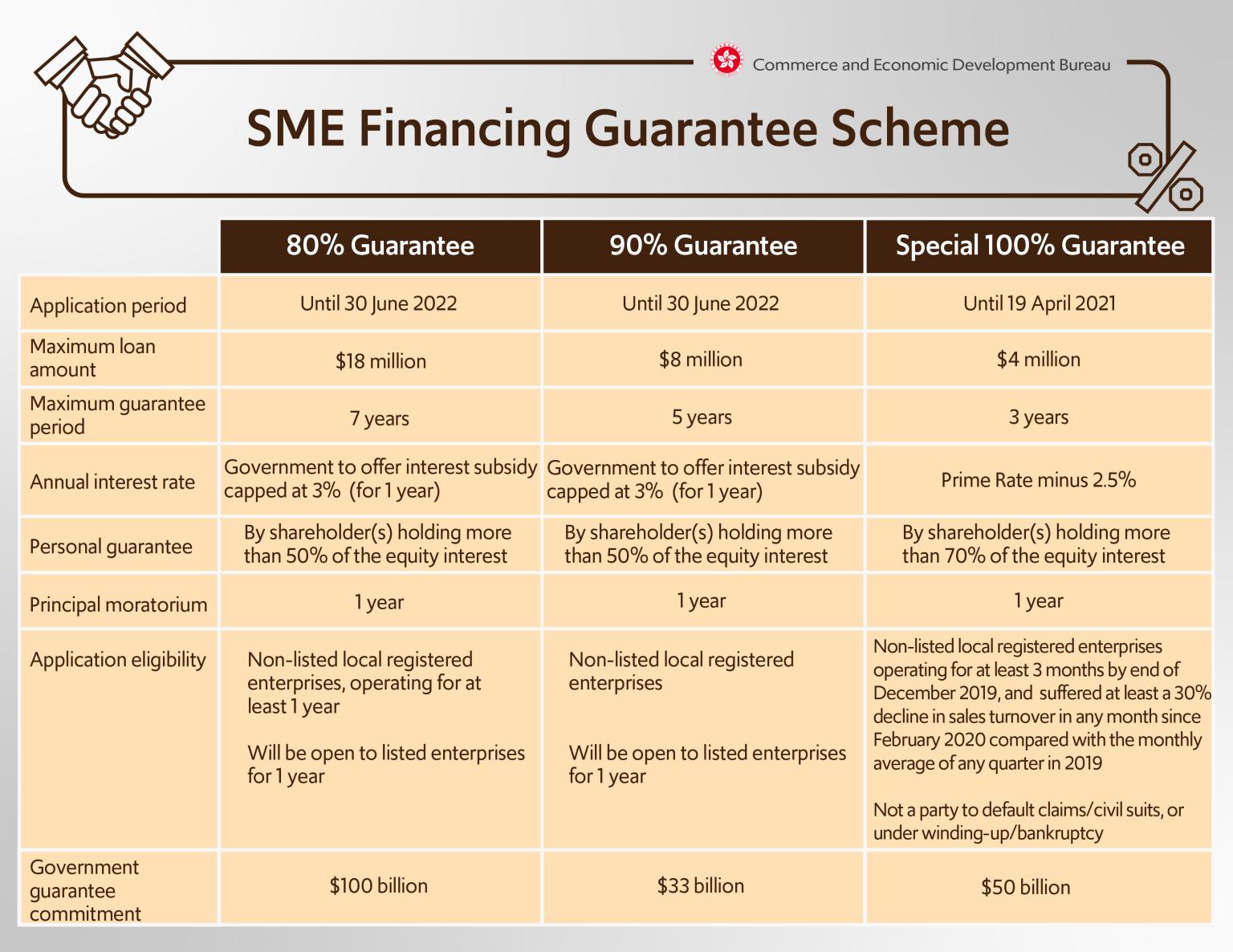

SME Financing Guarantee Scheme

Under the SFGS, HKMC Insurance Limited (HKMCI), which is a wholly owned subsidiary of the Government, may provide certain guarantee coverage for credit facilities of eligible enterprises approved by participating lenders. Using the additional funding, the Hong Kong Government is now guaranteeing 100% of loans of up to HK$4 million to SMEs at low interest rates.

Previously the Government offered 80-90% guaranteed loans, however banks were reluctant to lend to SMEs as this left them with some risk. The Government is now willing to offer a 100% guarantee, as similar loan guarantees offered during the SARS epidemic were not abused, according to Peter Shiu Ka-fai, who is the Hong Kong Legco member representing wholesale and retail.

Applications for the 100% Guarantee Loans scheme opened on 20 April 2020 and will close on 19 April 2021. Paul Chan made the announcement on 16 April 2020 in order to ease “the cash flow problems of enterprises adversely affected by COVID-19”. With this scheme the advantage is that, in case of a loan default, the guarantee is paid out directly from the Government budget and banks will bear no risk.

Banks will therefore be willing to provide widespread loans to struggling SMEs. The hope is that these loans will help keep business running as usual in Hong Kong and it is estimated to benefit about 20,000 to 50,000 SMEs.

Eligibility

In order to be eligible for this loan the enterprise will have to fulfil the following criteria:

- be a registered business under the Business Registration Ordinance, Cap. 310 that is regarded as being a substantive local business operation;

- regarded as an SME under the definition of the Government of Hong Kong SAR;

- not an associate of the lender;

- not a business lender.

What are the conditions?

The loans are available to all sectors. Enterprises will be eligible if they have been operating for at least 3 months since the end of December 2019 and have suffered at least a 30% decline in sales turnover in any month since February 2020, compared with their monthly average of any quarter in 2019.

Each enterprise will receive a loan amount equal to the total amount of employee wages and rents for 6 months, or HK$4 million, whichever is lower. The maximum repayment period of a loan under the guarantee is 36 months and enterprises will also have the option of applying for an optional principal moratorium for the first 12 month, which is a legal authorisation for debtors to postpone payment.

Proceeds from the loan may only be used for wages, rent and imminent working capital needs.

An interest rate of the Prime Rate minus 2.5% per annum (i.e. current interest rate at 2.75%) will be charged and all guarantee fees will be waived.

A condition of obtaining these loans is a personal guarantee made by the company owner(s). One or more company owner(s) will have to personally guarantee to repay the unpaid loan amount, if the company is unable to meet its financial obligations.

Sounds good? Right…….?

The requirement for a personal guarantee may be problematic.

The limited company structure is designed to keep the company’s liabilities and the owner’s liabilities separate; the personal guarantee means the company owner(s) has liabilities and may be at risk if the SME is unable to repay the loan.

Naturally, concern has been raised over this point.

Phil Aldrige, who chairs the SME and Start-up Committee for the British Chamber of Commerce in Hong Kong, has suggested that this requirement would create uncertainty among SME owners. If they receive a company loan and it defaults, their personal assets and credit rating will be at risk.

Implications of the personal guarantee

As a SME owner, making a personal guarantee may put yourself at significant risk. Before entering such a commitment, it is important you fully understand what you are letting yourself in for. The personal guarantee required for the 100% Guarantee Loan has the following implications:

- In the event of a default on the loan, the lender would typically look to the personal guarantee.

- If the SME and the personal guarantor(s) fail to make the payments after demand notices from the lender, normally the lender will have two options: 1) begin legal proceedings 2) petition for your bankruptcy. However, this loan is 100% guaranteed by the Government which means the lender will also be able to go to the Government to receive 100% of the loan amount back.

- A personal guarantee can be enforced by the Courts with the lender seeking to enforce a judgment against the guarantor’s personal assets.

- If a loan is not paid, both the company and the guarantors may well be taken to court. There may be legal grounds to challenge a creditor’s right to enforce a personal guarantee. It is recommended that legal advice is sought to assess any viable challenges to a creditor’s case.

You may feel confident now that your business will succeed in the future and there is limited risk on your personal guarantee, but, as highlighted by the recent pandemic, you do not know what is around the corner. As an owner of a SME, future loans/mortgages etc would be difficult to obtain.

It may be possible to get personal guarantee insurance, and this may minimise your risk should the worst happen. Whether this is practical and cost effective will depend on various factors, such as the enterprise’s financial stability, and the amount being guaranteed and the cost of the premium.

What if I already have a SFGS loan?

An enterprise is eligible for the 100% Guarantee Loan regardless of whether they have already obtained a loan under the SFGS. However, if a company already has a loan through the SFGS, it can only apply for further SFGS loans through the same lender.

Flexible loan arrangements

Many SME owners are seeking relief from their current loan obligations rather than another loan. They already have loans that they are paying off, another loan is not an answer to their problem.

The Hong Kong Monetary Authority (HKMA) have asked banks to consider more flexible loan arrangements. Banks have responded to this by introducing various measures, such as pauses on loan repayments and residential mortgages, extensions of loan tenors and converting trade financing lines into temporary overdraft facilities.

According to the HKMA, the granting of principal repayment holidays to SMEs have amounted to around HK$32 billion and the extension of loan tenors to SMEs have amounted to over HK$20 billion.

If you are an owner of a SME and you are struggling with your loan repayments because of COVID-19, contact your lender and see if these flexible loan arrangements are available to you.

Our take

There is no doubt that the SFGS will help SMEs in this time of need. Whether it is the most effective measure is another question and there are differing opinions on this point.

There may still be updates to come with the scheme, so it is important to stay updated and look out for any changes to the current set-up. For full information on the SME loan schemes please follow this link.

At Hugill & Ip, we have extensive experience in helping SMEs achieve their goals and navigating them through problems. If you own a SME and want more information and assessment of risks associated with financing schemes, such as the SFGS, please do not hesitate to get in contact.

At Hugill & Ip, we have extensive experience in helping SMEs achieve their goals and navigating them through problems. If you own a SME and want more information and assessment of risks associated with financing schemes, such as the SFGS, please do not hesitate to get in contact.

This article is for information purposes only. Its contents do not constitute legal advice and readers should not regard this article as a substitute for detailed advice in individual instances.