With the three-month period covered by the 1st tranche of the Government’s Employment Support Scheme (“ESS”) payments fast approach approaching, applications for the 2nd tranche of payments are set to commence from 31 August to 13 September.

Eligibility

The eligibility requirements remain the same i.e. all employers who have been making MPF or ORSO contributions, before 1 April 2020, with the exclusion of certain ineligible employers (for example, the Government and statutory bodies).

Employers that did not apply for the 1st tranche of payments are still able to apply for the upcoming 2nd tranche payments so long as they meet the eligibility requirements.

Successful applicants can expect to receive their subsidy within 3 to 4 weeks after the application has been submitted.

Self-employed individuals who have already received a one-off lump sum subsidy in the 1st tranche will not be able to apply for the 2nd tranche.

Available subsidy

The level of the subsidies remains the same: 50% of actual wages in the “specified month”, capped at HK$18,000 per employee per month. The subsidies will cover 3 months, from September to November 2020.

Again, the employer can pick the “specified month” for their subsidy calculation from the period from December 2019 to March 2020.

Headcount

As discussed in our article “Employment Support Scheme (ESS) Update”, headcount must not be reduced. The headcount will be assessed according to the company’s headcount in March 2020. This also applies to first time applicants who did not apply for the 1st tranche of payments.

If headcount is reduced, employers can expect to be penalised.

Penalty calculation

If there has been a reduction to the headcount during the period of the 1st tranche payments (June – August) then a penalty will be applied as follows:

Subsidies received for a particular month ($) x Headcount reduction percentage for a particular month (%) x Penalty percentage (%)

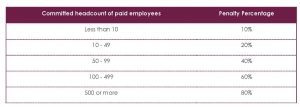

The penalty percentage is determined by the employer’s “number of committed headcount of paid employees” as follows:

Penalty Payment

The intention is for the Government to deduct any penalties from the 2nd tranche ESS payment.

The same rules will apply to any reduction in headcount (compared to March 2020) during the period of the 2nd tranche payments (September – October). However, since the Government has not announced any 3rd tranche measures, it is likely that any penalty incurred during the 2nd tranche would need to be repaid on demand.

Increased Penalties

The Government has, however, now included a warning that:

- (i) if there were substantial redundancies during the 1st tranche period (and there is no proof of attempts to re-hire) then the employer might be denied eligibility to participate in the 2nd tranche; and

- (ii) if there are substantial redundancies during the 2nd tranche period, the Government will seek to clawback part / all of the 2nd tranche payments.

There is no guidance as to what would constitute “substantial” redundancies. We don’t know if it will be measured by percentage of workforce or number of employees (or, possibly, a combination of both).

Undertakings

Employers must still undertake not to make redundancies during the subsidy period, and to spend all the wage subsidies on paying wages to the employees.

Additionally, major property management companies need to undertake to give back at least 80% of the amount equivalent to their wage subsides to the owners or owner’s associates. ParknShop and Wellcome need to undertake to provide more coupons and discounts to their customers.

Conclusion

Much remains the same with regard to eligibility and application process. If undertakings have been broken due to headcount reduction, this will give rise to penalties but, unless the reductions are “substantial” will not completely invalidate an employer’s entitlement to participate in the ESS. However, if redundancies become substantial then the Government has mechanisms to either deny 2nd tranche relief or claw back 2nd tranche relief.

If you would like to understand more on legal implications connected to Employment issues, you can contact the partner heading our Employment & Business Immigration practice – Adam Hugill.

This article is for information purposes only. Its contents do not constitute legal advice and readers should not regard this article as a substitute for detailed advice in individual instances.